Virtual Zone or International Company: Which Model Is More Effective for IT Business in Georgia

Association Representative Attended the “Women in Business and AI Technologies” Forum

June 4, 2026

First Half of 2026: Results and New Initiatives

July 28, 2026Virtual Zone or International Company: Which Model Is More Effective for IT Business in Georgia

When choosing an operating model in Georgia, IT companies typically consider two key frameworks: International Company status and Virtual Zone Person (VZP) status. Both offer significant incentives, however they differ substantially in terms of tax burden, operational requirements, and applicability.

Analysis of the 2022–2025 data leads to one important conclusion: the practical impact of these statuses differs not only in terms of their conditions, but also in their actual contribution to the economy.

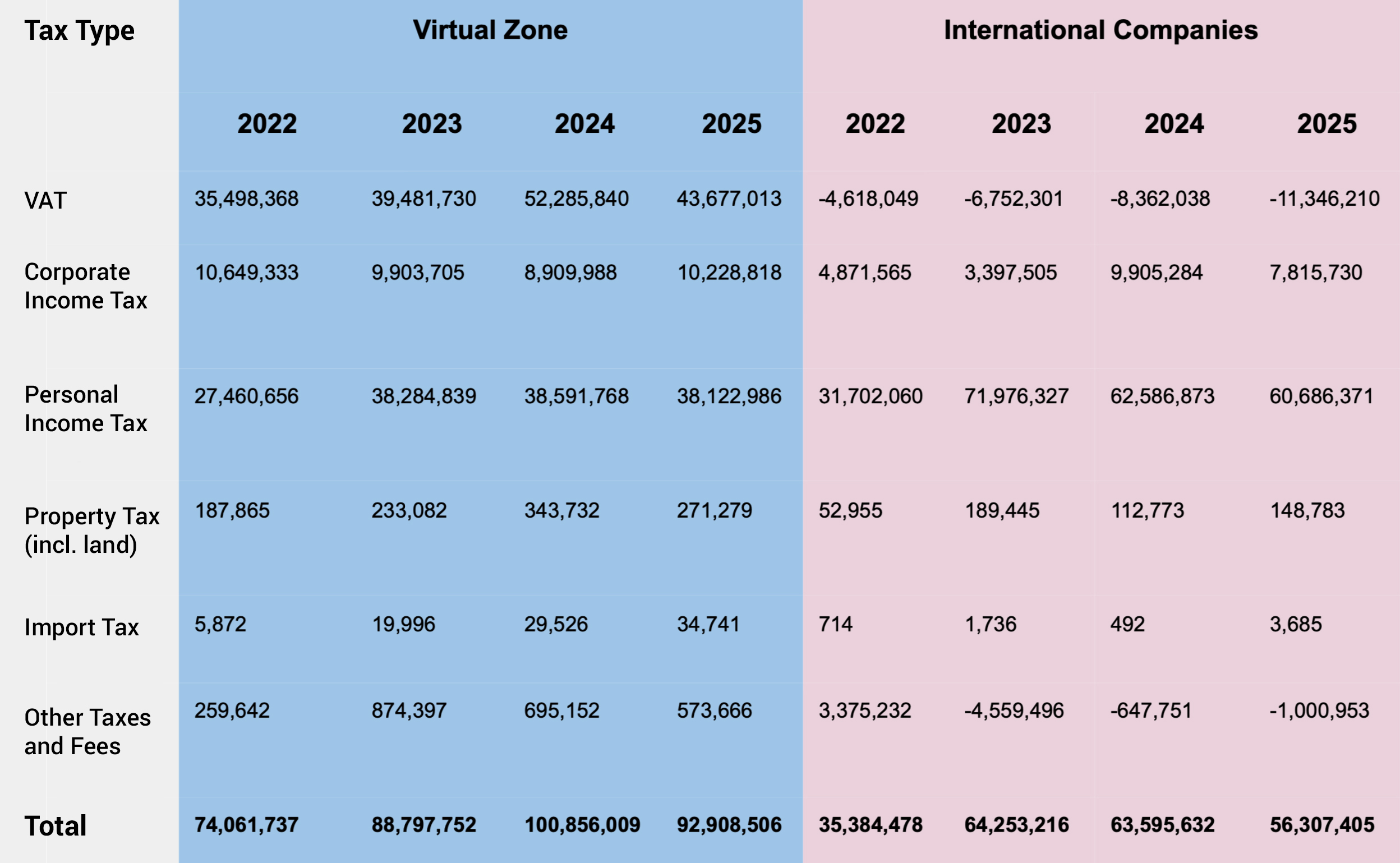

Total Contribution to the Budget

Virtual Zone companies (VZP):

2022: 74.1 million GEL

2023: 88.8 million GEL

2024: 100.9 million GEL

2025: 92.9 million GEL

International companies:

2022: 35.4 million GEL

2023: 64.3 million GEL

2024: 63.6 million GEL

2025: 56.3 million GEL

To provide an objective assessment of the effectiveness of each status, the actual structure of tax contributions is presented below (2022–2025).The data was provided by the Revenue Service of Georgia.

Tax Contributions Structure (2022–2025)

Note:

The data includes taxpayers who held either International Company status or Virtual Zone status for at least one day during the reporting period.

Negative values reflect tax refunds or carry-forward adjustments.

As reflected in the data, Virtual Zone companies consistently generate a higher overall contribution to the state budget of Georgia.

Tax Burden and Structure

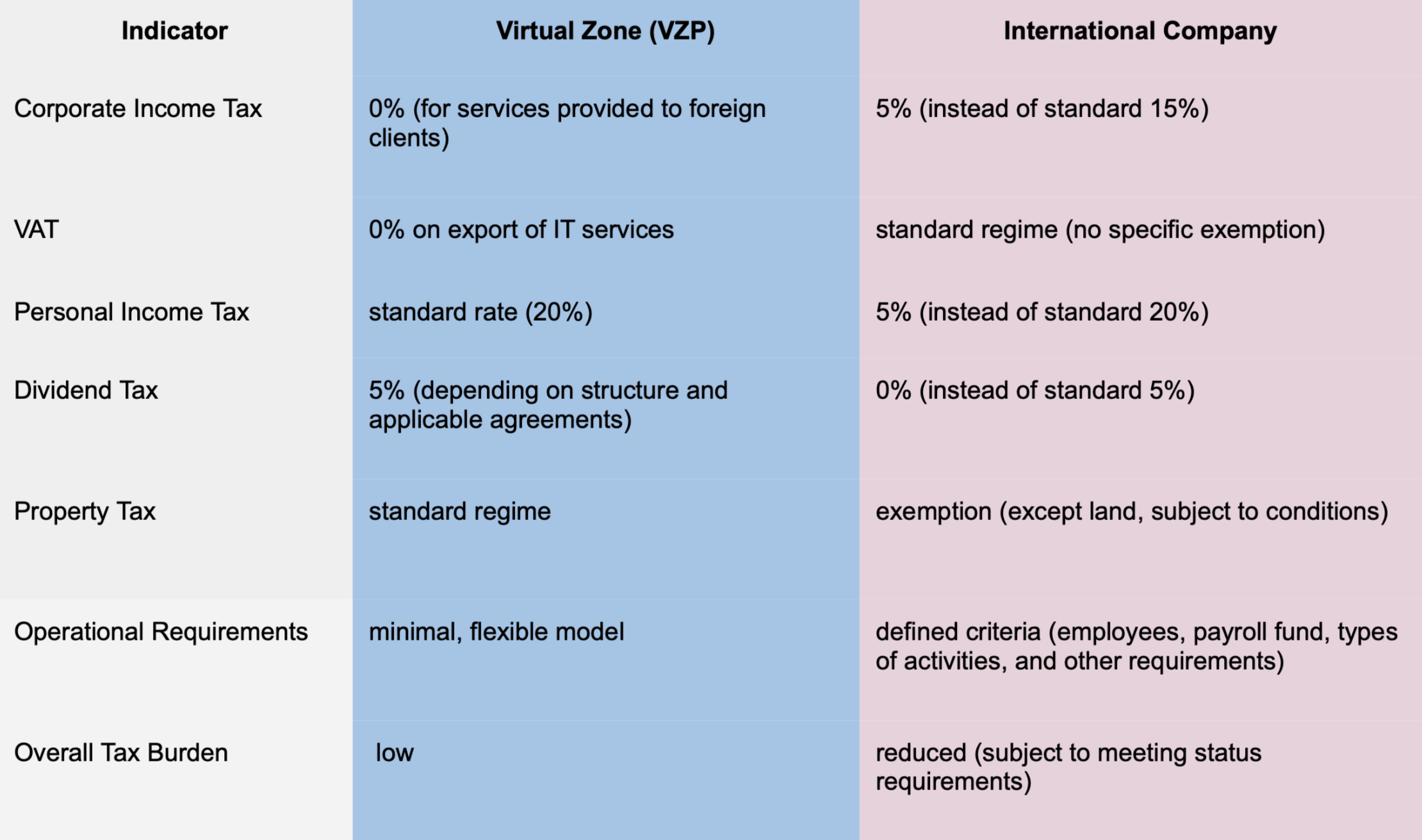

The Virtual Zone framework allows companies to significantly reduce their tax burden, particularly in relation to export-oriented IT services.

Why Virtual Zone Status Companies Generate a Significant Budget Contribution Despite More Favorable Taxation

Based on actual tax revenue data for 2022–2025, clear differences emerge in the tax base structure of the two statuses.

At first glance, more favorable taxation under Virtual Zone status would be expected to result in lower budget contributions. However, the actual data tells a different story.

According to the data presented: — Virtual Zone companies generate higher contributions across several tax categories, including VAT and corporate income tax — International companies, in turn, show higher personal income tax figures, reflecting differences in cost structures and business models

This points to a structural difference in the tax base between the two regimes.

The actual data shows that the favorable Virtual Zone status does not mean a reduced overall budget impact. On the contrary, despite a relatively low tax burden, this status generates significant and stable tax revenues.

Operational Requirements and Flexibility

The Virtual Zone status is characterized by a high level of flexibility:

— minimal requirements regarding staff and local presence

— no mandatory salary threshold requirements

— low entry barriers

— the ability to operate through distributed teams and export-oriented service models

The International Company status generally involves:

— a more substantial local presence in Georgia

— a significant payroll fund

— compliance with established activity criteria

— a more structured operational and compliance framework

Which Companies May Benefit More from Each Status

The Virtual Zone status may be an optimal solution for companies that:

— are focused on exporting IT services

— primarily work with clients outside Georgia

— use distributed teams or remote operating models

— do not plan to establish a significant local workforce

— seek to reduce tax and administrative burdens

Advantages of the Virtual Zone status include:

— 0% profit tax on services provided to foreign clients

— 0% VAT on exported IT services

— absence of minimum employee headcount requirements

— a flexible operational model

This status is frequently used by export-oriented IT companies due to its combination of flexibility and tax efficiency.

International Company status may be more applicable if:

— the company maintains a substantial presence in Georgia

— a large local team is being established

— payroll constitutes a significant share of operational costs

— the business includes a strong local operational component

— a more institutionalized business structure is important

Advantages of the status include:

— reduced personal income tax rate (5% instead of the standard 20%)

— 0% tax on dividends

— the ability to use a structured model suitable for larger organizations

This status is more commonly used by companies with a substantial local operational base and a significant number of employees.

Key Difference

The key distinction between the two statuses lies in the structure of tax optimization:

— in practice, the Virtual Zone status is often used for export-oriented activities due to the specific features of its tax framework

— International Company status is primarily aimed at reducing the tax burden associated with payroll expenses

Conclusion

An analysis of data for 2022–2025 shows that Virtual Zone status remains one of the most widely used and tax-efficient frameworks for export-oriented IT companies in Georgia.

For export-oriented IT companies, Virtual Zone status represents an effective balance between flexibility, tax efficiency, and operational resilience

Want to determine which model fits your business?

Contact us for an individual assessment.

info@viz.ge